Three phases of human-centered design

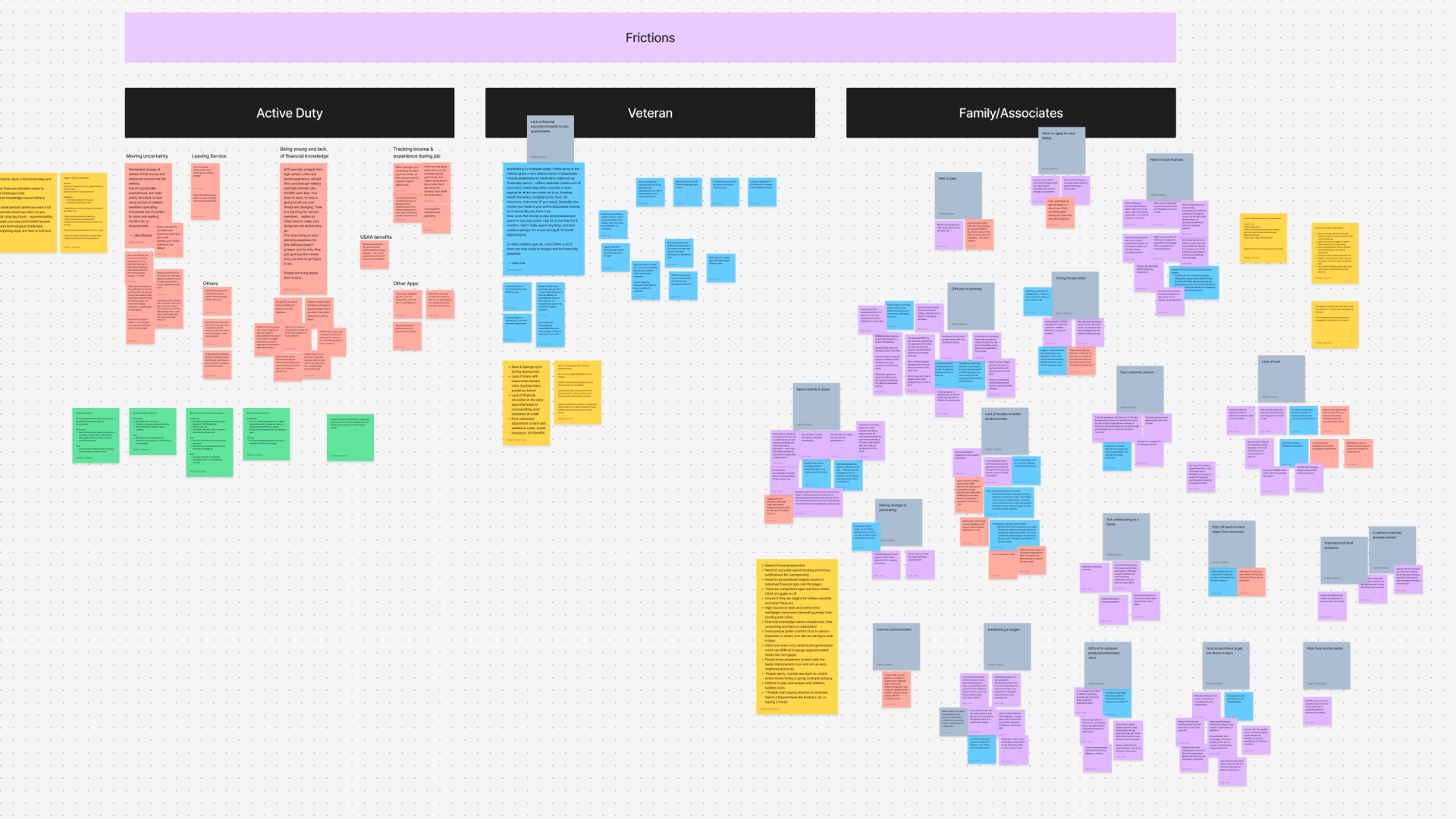

I partnered with the lead researcher to transform ethnographic interview findings into actionable insights, ensuring stakeholder alignment before moving into ideation. I then owned and led the design of 50+ assets for an immersion workshop: from journey maps and insight posters to stimulus cards and concept frameworks, while also supporting logistical planning to ensure a seamless experience.

Partnered with the researcher to surface key insights that informed the design approach, then took complete ownership of all 50+ visual assets for the immersion workshop.

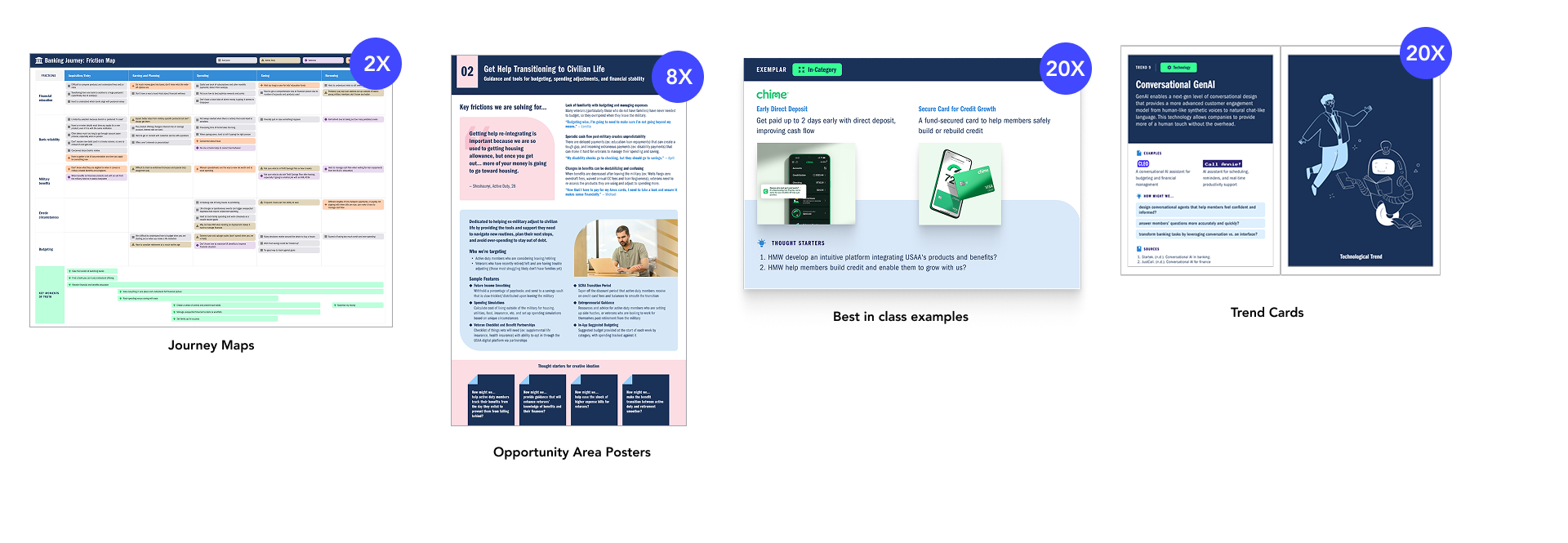

I facilitated sessions across a two-day in-person workshop with stakeholders, guiding them through user pain points, research findings, competitor analysis, industry trends, and best-in-class examples. From those sessions, I inspired the development of 10+ concept prototypes, refining them through real-time feedback and iteration. We then narrowed down to 4–5 strong directions through a structured voting process.

Led concept mockup creation for the next round of ethnographic testing. Synthesized key insights and designed refined concept mockups that translated stakeholder thinking into testable prototypes.

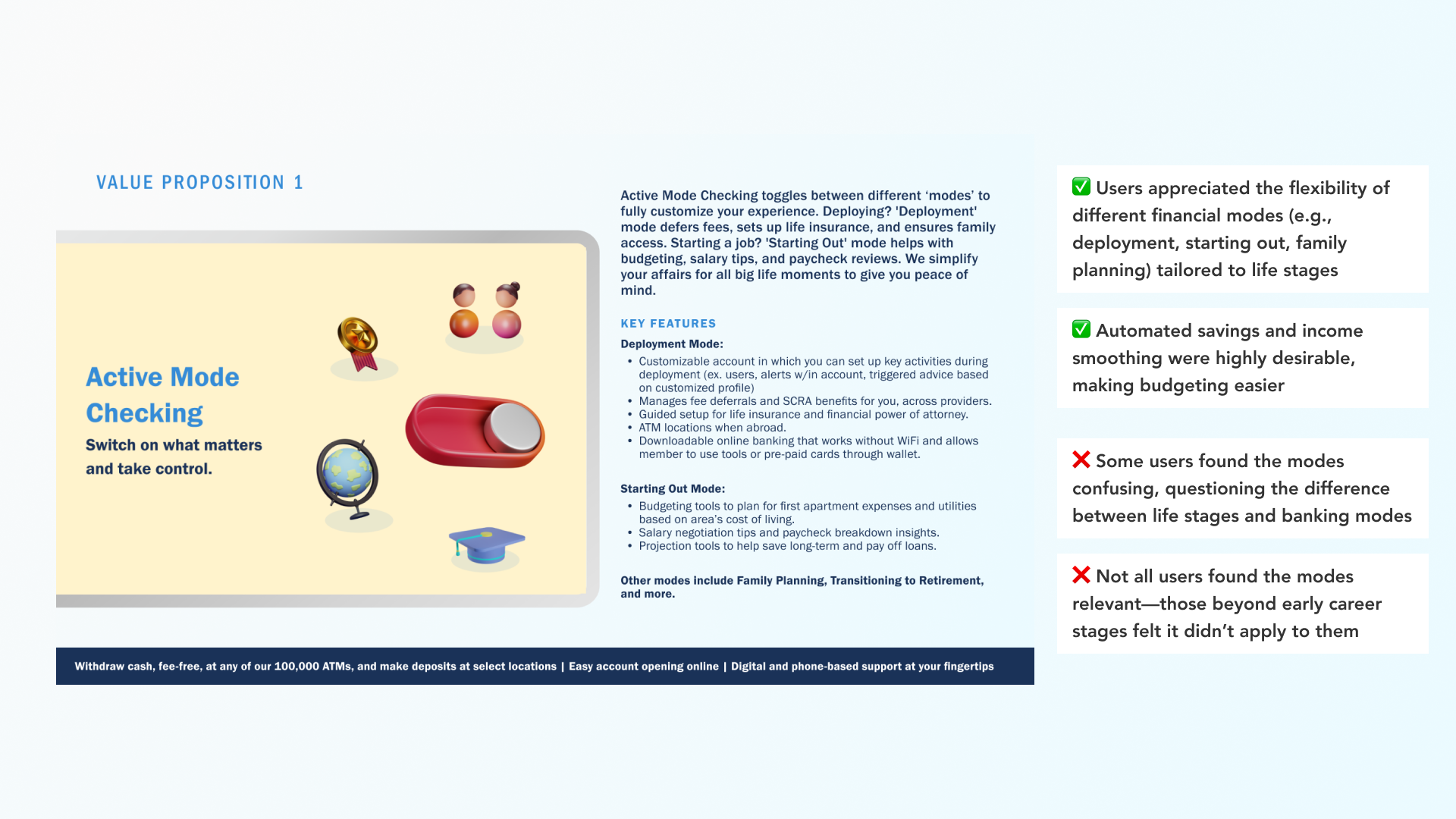

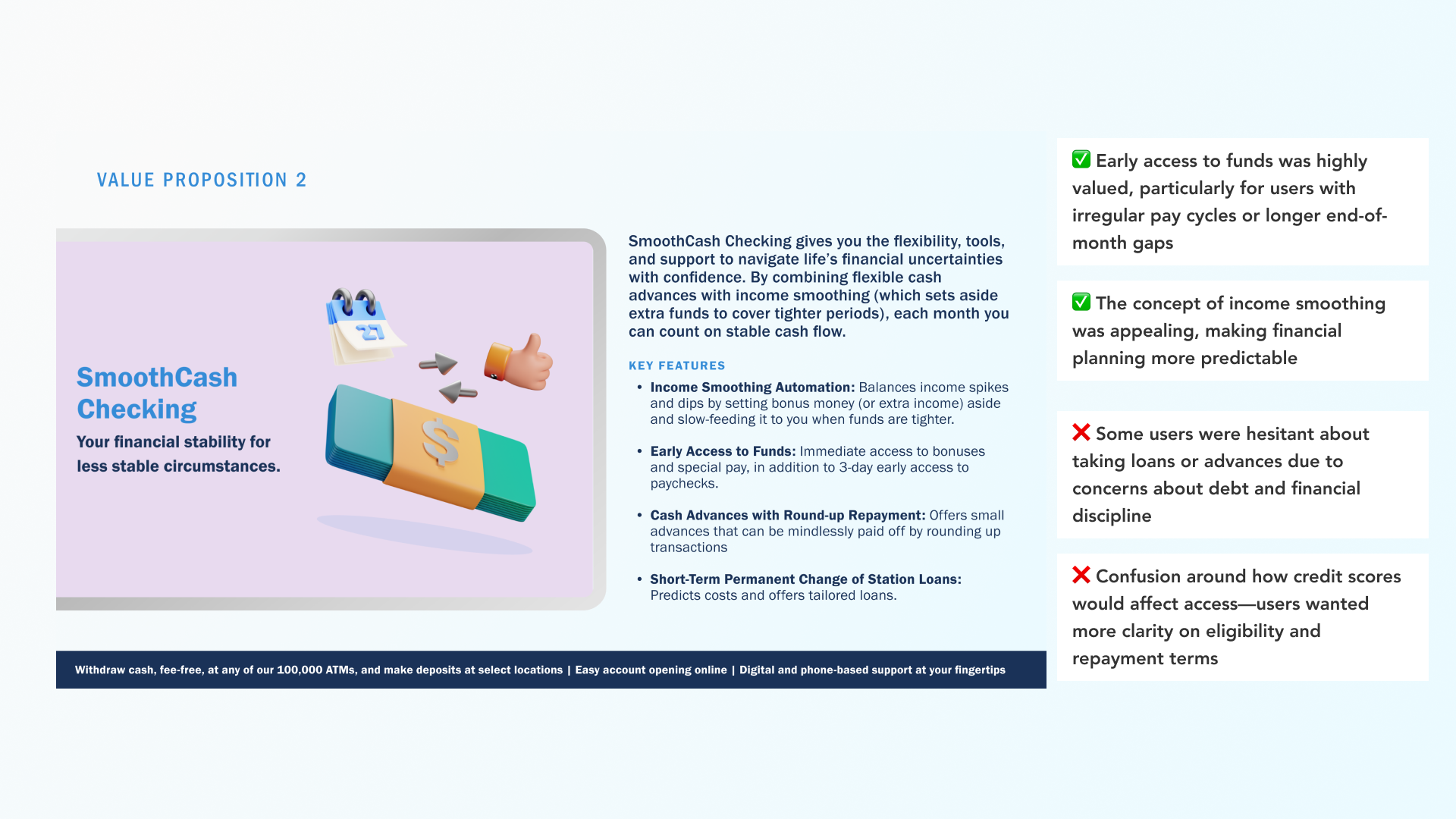

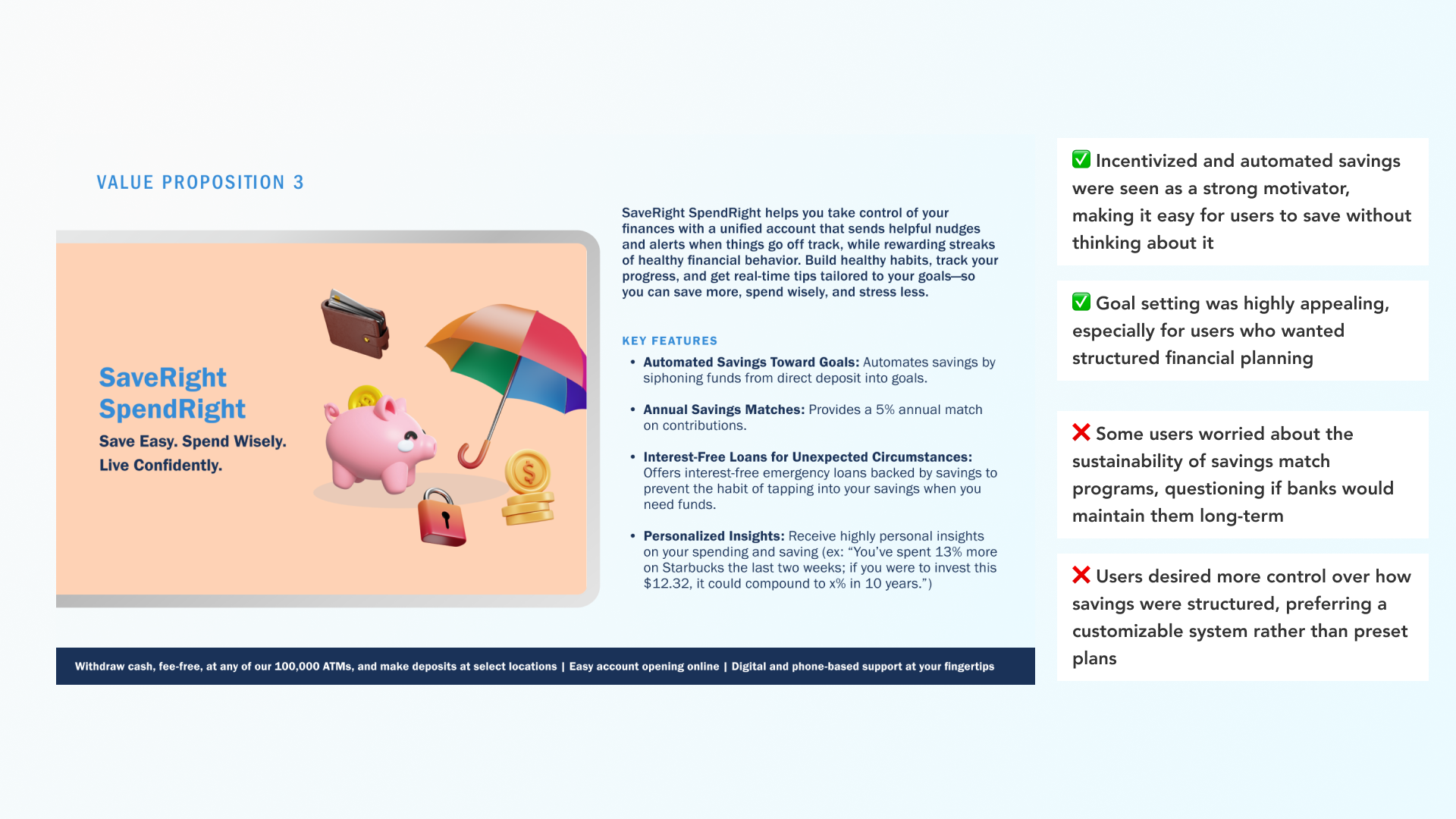

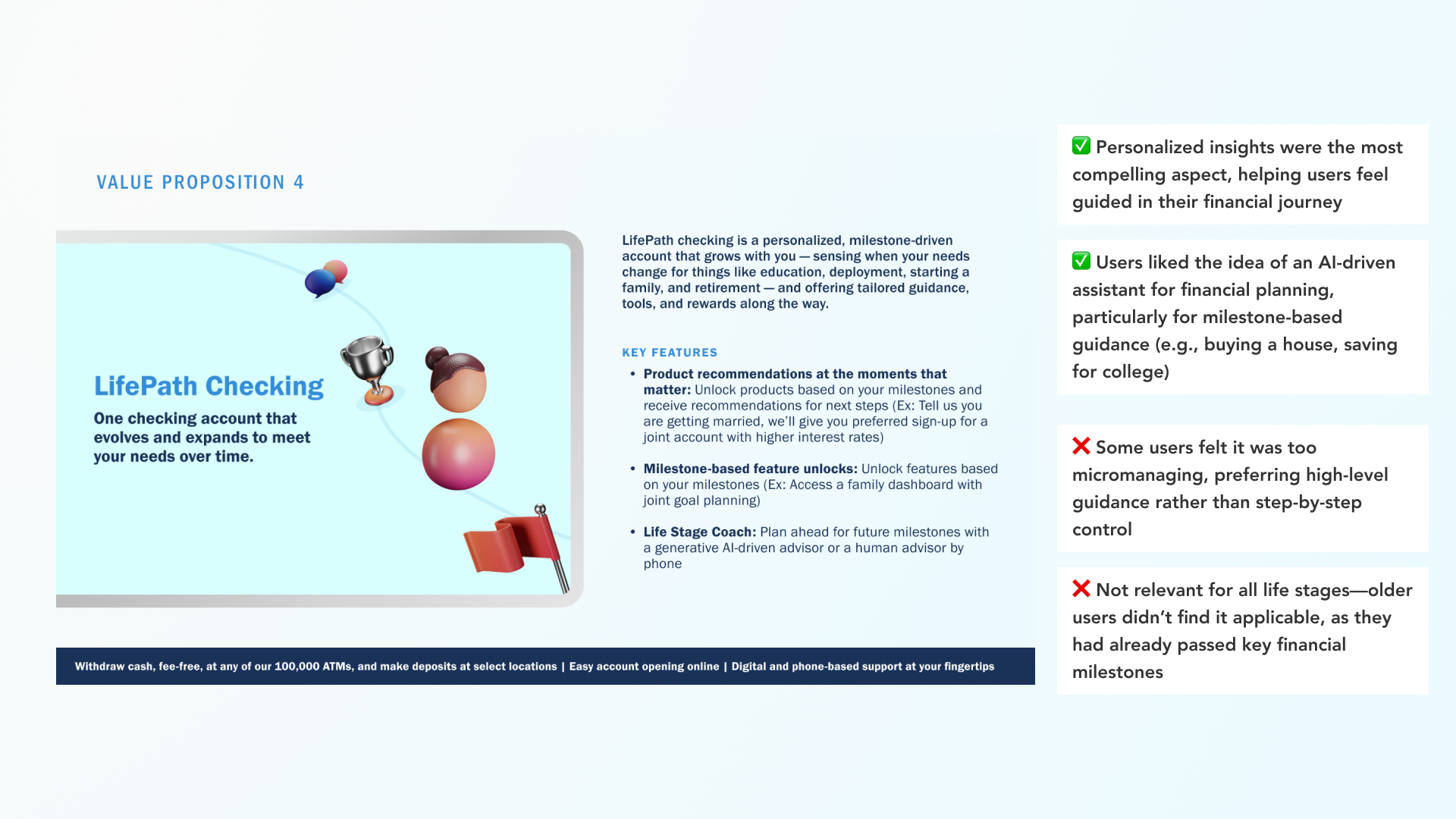

With 4–5 high-impact concepts shortlisted, I created low-fidelity prototypes to test usability and concept desirability before investing in high-fidelity design. I then conducted iterative testing sessions with 6+ real users across Active Duty, Veteran, and Family/Associate segments, refining concepts based on behavioral insights and usability feedback until we had a clearly validated direction.

Led the design of all low-fidelity prototypes and conducted 6+ testing sessions across user segments, synthesizing findings into refined concepts ready for the next phase of investment.